Trouble brewing in Malawi

An attempt to shield voters from inflation through exchange-rate controls backfired

In April 2024, Malawi’s government, led by President Lazarus Chakwera, made a telling decision that revealed its true economic priorities. With elections approaching, the Reserve Bank of Malawi (RBM) reversed an IMF-mandated devaluation and fixed the official exchange rate. The logic was straightforward: devaluation was pushing up import prices, import prices were fuelling inflation, and inflation was losing votes.

Fix the rate, shield consumers, win the election.

Chakwera lost anyway. In September 2025, voters chose his predecessor Peter Mutharika by a landslide — 56.76% vs. 33.01% of the vote — with the economy as the dominant issue. The exchange rate fix had failed even on its own political terms, and left behind a structural wreckage that Mutharika now inherits.

This is not primarily a story about one government’s cynical monetary policy, but rather a story about what happens when a state tries to use an exchange rate anchor it cannot actually sustain.

The mechanics are worth understanding. When Malawi re-fixed its rate, it created an immediate gap between the official rate and the parallel market, which was running roughly 100 per cent above official for essential goods at its peak. This is not an abstract distortion. It meant that ordinary import-dependent households — the vast majority of the population — were being pushed onto a black market to access basic goods, while the formal rate offered them nothing.

Meanwhile the tobacco sector, which benefits from periodic step-devaluations and conducts dollar-denominated transactions, remained largely insulated from the kwacha (Malawi’s currency) depreciation eroding household purchasing power. Yet even here, the desperation of the FX position is visible: the RBM imposed a 30 per cent export surrender requirement to claw back foreign exchange from its primary beneficiaries, imposing distortions even on the sector the arrangement was designed to protect. The fix looked like consumer protection. It functioned as a subsidy to export capital at the expense of import-dependent labour.

Credible exchange rate commitments require transparency, enforceability, and sufficient political cost of abandonment. Malawi’s arrangement failed all three. The Reserve Bank published no intervention data, giving private actors no basis for confidence in the rate. The government's willingness to re-fix the exchange rate after already agreeing to float under IMF Extended Credit Facility conditions demonstrated that the commitment could be abandoned on demand. And the ECF terminated without completing a single review, removing the one institutional constraint that gave the arrangement any external credibility. With gross reserves at just 0.7 months of imports — far below any recognised adequacy threshold — the Reserve Bank was not defending a rate so much as declaring one.

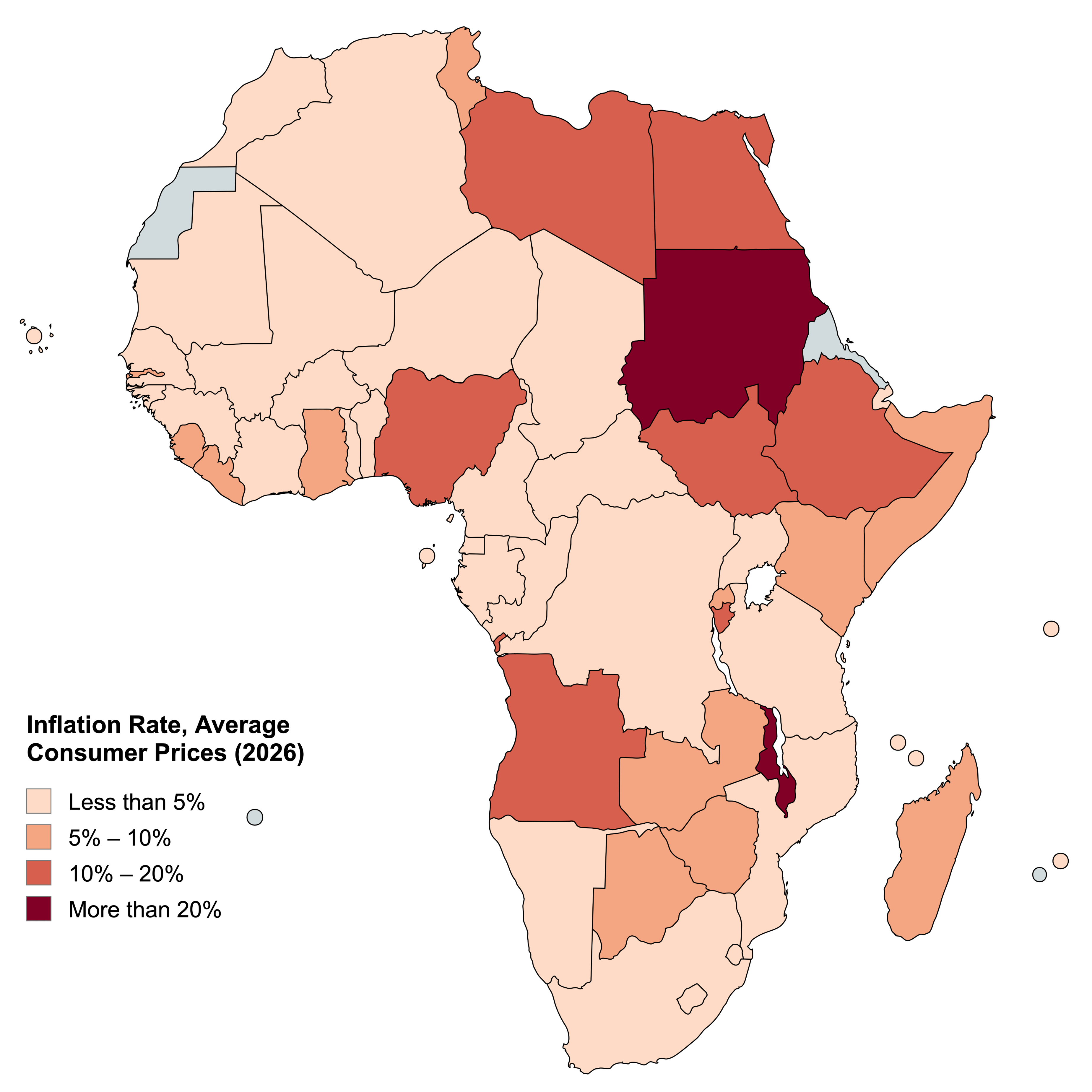

The consequences were predictable. Inflation peaked at 35 per cent in early 2024 and has since fallen to around 24 per cent as of early 2026 — a sign of some stabilisation — but still deeply damaging for a country where nearly three-quarters of the population lives below $2.15 a day as of 2025. The parallel market spread deterred foreign direct investment not only because of Malawi’s underlying economic weaknesses, but because investors could not reliably assess effective returns when profit repatriation might occur at either the official or the parallel rate. The currency distortion was generating uncertainty on top of genuine economic weakness, compounding both.

The IMF’s prescription — a unified market-clearing rate — is technically correct. The problem is that it is insufficient on its own. Malawi arrived at this crisis through a combination of fiscal dominance, reserve depletion, and absence of genuine central bank independence. A rate unification that is not preceded by fiscal consolidation, reserve rebuilding, and meaningful RBM autonomy will simply face the same political pressures that have hampered every previous stabilisation attempt. The structure that produced the April 2024 decision has not changed. Only the government has.

Mutharika inherited an economy where public debt has returned roughly to the levels that preceded Malawi’s major debt relief in 2006, in which the ECF remains terminated, and in which the distributional coalitions that benefit from exchange rate distortion are still politically powerful. The tobacco sector’s interests have not changed. The political incentives to prioritise short-term price stability over long-term monetary credibility have not changed. The question is whether a new government, without an electoral horizon for another four years, has the window to do what its predecessor could not.

There is a narrow case for cautious optimism. Chakwera’s loss demonstrated that economic mismanagement carries electoral consequences; the electorate delivered the punishment the IMF’s terminated programme could not. Mutharika has both the political capital of a landslide and the institutional memory of having governed before, providing a rare political window for change. The interest rate cut from 26 to 24 per cent in March 2026 is modest but suggests a willingness to begin normalisation. Yet these advantages are opportunities rather than achievements. The underlying constraints — weak reserves, high debt, and powerful interests that benefit from distortion — remain largely unchanged.

Optimism has to be conditional on the sequencing being right. Rate unification without fiscal consolidation is not reform; it is exposure. Malawi’s monetary problem is downstream of its fiscal and institutional problems, and treating the exchange rate in isolation will not resolve it.

The IMF knows this.

The question is whether the new government does too, and whether it has the political appetite to act on that knowledge before the next electoral cycle begins to foreclose options once again.

| A guest post by

|